08

Jul

Beyond Coronavirus – the 2020 Economic Outlook

in General

Comments

(Updated 8 July 2020, first published 10 April 2020)

If during the first quarter of the new decade you felt like a character in a Stephen King novel, you wouldn’t be alone. Unfortunately, for the majority of us around the world, the horror story looks set to continue, or possibly get even worse in the short term.

Not only are we seeing the tragic effects of the virus as it infects human beings, but also the damage it is causing to the foundations of world trade, individual economies and, once again, as if ill health is not enough of a burden, impacting us all by threating our livelihoods.

Just about the only positive news we’ve heard in recent weeks is that China, often described as “the world’s factory”(in 2018 it accounted for 13.5% of world exports and 11.4% of imports by US$ value), is said to be now slowly getting back to work.

The impact this pandemic has had on stock markets around the world has been a constant feature in daily news bulletins, the falls reflecting investors’ lack of confidence in future economic growth , their doubts about the performance of governments and the effectiveness of the action taken in responding to the spread of the virus.

Some sectors have been hit far worse than others, transport suffering most obviously as a direct result of restrictions applying to almost all modes of travel, especially airlines. Manufacturing around the world is also badly affected, caused by the massive disruption to supply chains.

As a consequence of the actions taken to curb the spread of coronavirus, the so-called “flattening of the curve”, the consequential reduction in economic activity has shown itself very noticeably in employment statistics. Taking the US as an example, the employment rate had been steadily climbing over the last ten years. In a press release issued yesterday (9 April 2020), the US Department of Labor said that initial claims for unemployment insurance in the week ending 4 April was an astonishing 6.6m (many of the claimants had previously been working in the hospitality sector), adding to the 10m who registered in the two weeks before that.

Coronavirus is aggravating a situation that was already suffering a downturn, an important contributory factor being the US-China trade war, with tit-for-tat tariffs being imposed by both countries over the last two years. Back in January the future had started to look a little brighter with the easing of tension between the two. After months of negotiations the “Phase One” Trade Agreement was reached, although more limited in scope than many had hoped for, at least it was a step in the right direction.

Given what has happened up until now, what does the future hold in terms of how and when we will eventually recover from what the UN Secretary General has described as “the biggest challenge for the world since World War Two”?

The answer to that question lies firmly in the hands of individual governments around the world and the measures they take to first move us out of shutdown and then what they do to revive individual economies. Another significant unknown to add into the mix is whether or not the actions of those governments will be in any way co-ordinated. Hopefully they will be, although this is far from certain.

Pre-coronavirus we had been experiencing a shift from globalisation to nationalism. This weakening of international co-operation contributed in turn to our lack of preparedness and inability to co-ordinate an effective global response to the spread of coronavirus.

…a unique situation

We are actually now in a unique situation without any previous experience to learn from. Such prior knowledge would ordinarily have brought some reassurance to governments when trying to decide on the measures needed to kickstart their economies. Previously, economic downturns were usually brought about by lower aggregate demand, occasionally on the supply side, such as through geopolitical tensions. To address such scenarios, the various tools available and their suitability had already been tried and tested. For example, a cut in interest rates, or quantitative easing when rates were too low to allow this, or a reduction in taxes or an increase in government spending. Each individually, or a combination of two or more were often sufficient to revive an economy.

This downturn is unusual in so far as it has come about through a forced reduction in economic activity, designed specifically to reduce the rate of infection and thereby reduce the impact the virus has on already overstretched and, in many cases, underfunded health services. Still unknown is quite when is the best time to lift a lockdown – stimulate demand too early and the danger is that infections re-appear before a vaccine is available, or indeed before we actually know whether having coronavirus once makes an individual immune once fully recovered from infection.

…prevent long term damage

The approach taken by many governments thus far has therefore been to try to prevent longer term damage to the supply side of the economy. We see this for example in the support packages provided by the UK government, in terms of loan schemes for SMEs, rates relief and tax holidays for certain sectors and individuals, an 80% guarantee of income for those employees “furloughed”, as well as a reduction in interest rates to assist those businesses reliant on debt funding. All of these measures are expensive and need to be financed. As yet their likely final cost can only be, at best, guesswork. The UK recently has reportedly put in place a US$ 39billion package. How accurate this number turns out to be depends on how long the shutdown lasts and how many people, for just one aspect of the package, claim income support. If a three week lockdown turns into six and the number of claimants is double what had been forecast, then the final cost will be substantially more.

How these measures are paid for has also to be decided. The slowdown in the economy as a result of a shutdown will have already significantly reduced the current level of tax receipts. It does not seem unreasonable to assume that future generations of taxpayers will bear a significant portion of this burden, which in turn will adversely affect the future rate of economic growth. Financing using monetary measures, such as issuing government bonds, will no doubt also be one of the ways used to cover the fiscal measures now in place. Indeed this is the method being used in the UK at the present time, the Bank of England undertaking to fund the Treasury’s current package.

Precisely where each country is currently in the coronavirus cycle as well as the steps its government is taking and will take, to first reduce the spread, then to protect and revive the domestic economy, means there exists vast uncertainty about the future, making it difficult to forecast what will happen even at the individual country level. Predicting the effect this will have on world trade in the coming months and years is therefore many times more difficult, combining multiple uncertainties many times over.

…what do the experts say?

It would therefore seem sensible to take a look at what the experts on international trade are saying and consider each of their forecasts for the near future. Unfortunately none make for reassuring reading.

On 8th April 2020, the World Trade Organisation (WTO) issued a press release headlined: “Trade set to plunge as COVID-19 pandemic upends global economy”. In it they state that, in their opinion, “world trade is expected to fall by between 13% and 32% in 2020 as the COVID 19 pandemic disrupts normal economic activity and life around the world”. Note the range: 13% to 32%, reflecting the uncertainty they feel exists with respect to the scale of the impact.

None of us know when the current lockdown conditions will be eased, other than that for each of us they will be different, depending on which country you live in and at what stage the spread of the virus has reached. However, what we do know for certain is that the threat of cybercrime was already growing month on month, year on year. This growth is now accelerating, given the opportunities presented to criminals from millions of people now working remotely. Now more than ever, it is essential that organisations and their staff are aware of the threats and that systems are in place to protect them from damage and losses that could lead to the destruction of whole organisations.

The two scenarios they envisage account for the huge spread of possible outcomes in their forecast. One relatively optimistic, with a recovery assumed to start in the second half of 2020 (and taking us back close to the previous trajectory), the second being pessimistic, with a prolonged period of recovery,. Under both scenarios, certainly what we can conclude is that all regions (other than those reliant on exporting energy products, which have been relatively unaffected thus far, such as in the case of the Middle East) will suffer at least double digit reductions in their exports and imports in 2020.

The International Monetary Fund (IMF) said it expects a global recession this year that will be at least as bad as the downturn during the financial crisis more than a decade ago, followed by a recovery in 2021. In response they say they “stand ready to deploy all our US$1tn lending capacity”. As for a forecast of the scale of the downturn, all they would offer in March was “how far it falls, and how long the impact will be, is difficult to predict”, with the observation that it depends on how the epidemic develops, and the timeliness and effectiveness of policymakers’ actions.

Since making that statement, the IMF has published their World Economic Outlook for April 2020. The report is still understandably couched in terms of significant uncertainty, but on the assumption that the pandemic recedes in the second half, global growth for 2020 is forecast to be minus 3%, down 6.35% compared the forecast made in January 2020. In 2021 global growth is forecast to recover to a positive 5.8%, subject to the measures taken to avoid extended job losses and bankruptcies being successful.

However, if the pandemic does not recede in the second half, global GDP would be expected to fall even further, an additional 3% if it continues to the year end. If there is a longer outbreak in 2020 plus a new outbreak in 2021 the IMF forecasts global GDP could fall by an additional 8% compared to the baseline 5.8% for 2021, i.e. minus 2.2%. Even worse still would be the scenario whereby additional public debt “spooks the markets”. The increase in borrowing costs that result might then prevent countries providing the support that underlies the above forecasts.

On 24 June 2020 the IMF released their latest World Economic Outlook update. With the same provisos as for earlier reports, namely the forecasts are subject to “higher than usual degrees of uncertainty”, the projections in the latest report are more pessimistic than previously: a “more severe economic fallout than anticipated”.

This time global growth for 2020 is projected at minus 4.9%, compared to the previous 3.0% contraction, the global pandemic having a more serious impact on the global economy than last anticipated.

Persistent social distancing, greater damage to supply chains, and reduced productivity from enhanced safety and hygiene practices have impacted those economies with reducing infection rates. For those not in that “fortunate” position, extended lockdowns continue to reduce output.

Once again, the need for multilateral co-operation, the resolution of international trade and technology tensions and assistance regarding debt relief and financing are all stressed as being essential for recovery to be achieved within a reasonable time.

The OECD issued an interim Economic Assessment on 2 March 2020 in which they made their own observations at that point in time on the impact coronavirus might have on the world economy. An added complication when it comes to making forecasts is the fact that we have a moving target. For example, at that time the number of infections globally was around 90,000 with just over 3,000 deaths, mainly in China. As of today (10 April 2020), the figures stand at 1.6m cases and nearly 96,000 deaths worldwide. The OECD projections were then based on the assumption that the spread would be “mild and contained”, they said this would result in a drop from the 2.9% growth in 2019 to 2.4% in 2020. Unfortunately, this has been nothing like what has actually happened.

The OECD Secretary General made a further statement on 26 March, this time their estimates showed that “the lockdown will directly affect sectors amounting to up to one third of GDP in the major economies. For each month of containment, there will be a loss of 2 percentage points in annual GDP growth”. Again, they qualified their forecast by saying that making predictions was understandably difficult in a rapidly changing environment, and went on to state that the “initial direct impact of the shutdowns could be a decline in the level of output of between one-fifth to one-quarter in many economies, with consumers’ expenditure potentially dropping by around one-third. Changes of this magnitude would far outweigh anything experienced during the global financial crisis in 2008-09. This broad estimate only covers the initial direct impact in the sectors involved and does not take into account any additional indirect impacts that may arise.” They adopted the same mantra that actual GDP growth will be affected by the scale and length of each country’s shutdown, the medium term effects this has on demand for goods and services, as well as the nature and speed of implementation of the policies each country adopts to stimulate individual economies. It will also depend on how successful are the policies introduced to protect the economy during each shutdown.

On 10 June 2020 the OECD released a further update on its Economic Outlook, the first line being “the global outlook is highly uncertain” despite the pandemic starting to recede and activity pick up again.

The current Economic Outlook considers two alternative scenarios:

1. the virus continues to recede and remains under control, and

2. a second wave erupts later in 2020

“Both scenarios are sobering, as economic activity does not and cannot return to normal under these circumstances. By the end of 2021, the loss of income exceeds that of any previous recession over the last 100 years outside wartime, with dire and long-lasting consequences for people, firms and governments.”

As with the World Bank Report on 8 June 2020 (see below), the OECD believes recovery cannot be achieved without more confidence at both national and international levels, something that will itself not recover without global co-operation. Similarly global co-operation with respect to a future vaccine and its distribution is essential, without which the threat of a return of the pandemic will remain, thus undermining confidence and the willingness to invest.

The OECD concludes it latest report noting that the cost of bringing the pandemic under control has been frozen business activity in many sectors, widened inequality, disrupted education and undermined confidence in the future; economic recovery remains highly uncertain and vulnerable to a second wave of infections; and “with or without a second outbreak, the consequences will be severe and long-lasting.”

In the latest World Bank regional report (South Asia Economic Focus) released on 12 April 2020, the forecast is that regional growth will fall to between 1.8% and 2.8% in 2020. The worst performance in the last 40 years, 2020 growth had previously been projected to be 6.3%. The 2021 projection is for between 3.1% and 4%, down from 6.7% estimated previously. Once again, the report is qualified, warning that in the worst case scenario, where lockdowns are “prolonged”, the region would experience negative growth in 2020.

On 8 June 2020 the World Bank published its Global Economic Prospects Report which assesses the impact of the coronavirus pandemic and looks at the various possible courses of action and outcomes.

The baseline forecast envisages the deepest global recession since World War II, and whilst describing its own commitment and the need for appropriate individual policies at the country level, the World Bank states clearly that global co-ordination and co-operation will be critical to recovery.

The latest (baseline) forecast is for a 5.2% contraction in global GDP in 2020, “the deepest global recession in eight decades, despite unprecedented policy support” and “output of emerging market and developing economies (EMDEs) is expected to contract in 2020 for the first time in at least 60 years”.

Due to the sudden stop in human interactions, the result of lockdowns around the world, the unprecedented weakening of services-related activities will contribute to the record fall in global trade and oil consumption, with global unemployment rising to its highest levels since 1965, when available data began.

Due to such unusual degrees of uncertainty, the World Bank presents three possible growth trajectories for 2020-21. The baseline forecast is at 5.2% as above, whereas the downside scenario is based on the assumption of continuing flareups necessitating continuing control measures such as school and business closures, these remaining in place through Q3 of 2020 in many countries. In contrast the upside assumes rapid fiscal and monetary policy responses that will support confidence leading to a prompt normalisation of domestic economic activity, thereby releasing pent-up demand.

With the baseline suggesting a 5.2% contraction in 2020 of global GDP. The downside scenario predicts this figure will increase to 8%, as an additional three months of lockdown measures take their toll. If pandemic control measures are largely lifted by the close of Q2 and a sharp economic rebound gets underway quickly as businesses re-open and travel restrictions are ended, then global output might contract by about 4% in 2020. For more information, including forecasts by regions, download the full report.

FitchRatings released their third update of their Global Economic Outlook forecast on 22 April 2020, cutting still further their global GDP forecasts. They now expect world GDP to contract by 3.9% in 2020, twice as large as their forecast decline made in early April, and twice as severe as the 2009 recession.

In their Spring 2020 Economic Forecast released on 6 May 2020, the European Commission forecasts an uncertain recovery following a “deep and uneven recession”. It is projected that the EU economy will contract by 7.5% in 2020 and then grow by approximately 6% in 2021. In other words, the EU economy is not forecast to make up for the 2020 losses by the end of 2021. Compared to the 2019 forecast this represents a downward revision by around 9%. Not only will each member state’s recovery depend on how and when it can emerge from lockdown but also, given the interdependence that exists between member states, individual economic performance will also be affected by developments in neighbouring states.

Paolo Gentiloni, European Commissioner for the Economy, said: “Europe is experiencing an economic shock without precedent since the Great Depression. Both the depth of the recession and the strength of recovery will be uneven, conditioned by the speed at which lockdowns can be lifted, the importance of services like tourism in each economy and by each country’s financial resources. Such divergence poses a threat to the single market and the euro area – yet it can be mitigated through decisive, joint European action. We must rise to this challenge.”

Unemployment in the EU is expected to rise from 6.7% in 2019 to 9% in 2020, falling thereafter to around 8% in 2021. Inflation is expected to fall to 0.6% in 2020 rising to 1.3% in 2021, the fall this year the result of lower demand and lower oil prices.

Released on 7 July 2020, the European Union Summer Forecast reflects the impact of a slower lifting of lockdowns than had been anticipated in the Spring Forecast. As a result economic activity is now forecast to be even lower. The EU 2020 economy is now forecast to contract by 8.3% and grow by 5.8% in 2021 (the Spring Forecast was 7.5% and 6% respectively). The forecasts come with the usual warning that the future is far from certain, a second wave of infections being a serious risk – they are based on the assumptions of continual gradual lifting of lockdowns and no second wave of infection. On a more positive note, data appears to show recovery is now starting as we move into the second half of the year. However, reference is also made to potentially lower growth for the UK if it fails to secure a deal with the EU.

…one single example

To appreciate the effect on an individual economy, on 9 April 2020 the BBC in the UK reported on the enquiries it had made of fourteen UK economists, asking them to estimate the fall in UK GDP during the second quarter 2020. The results range from minus 7.5% through to 24%. To put this into context, quarterly figures normally only move by fractions of a percent.

Sir Charles Bean, an LSE Economics professor and member of the UK Government’s Budget Responsibility Committee (OBR), was quoted as saying that it was not implausible for a three month lockdown to knock “something like 6-8 percentage points off annual GDP”.

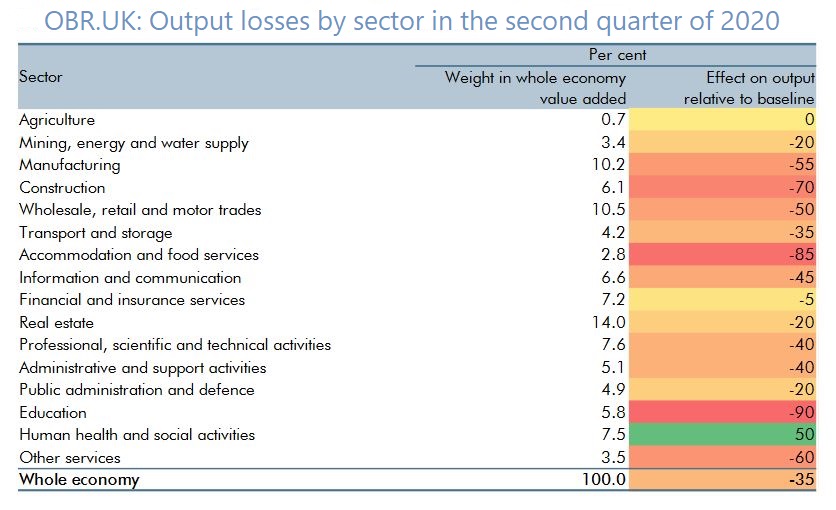

The OBR published its own forecast on 14 April 2020 of the impact coronavirus could be expected to have on the UK economy. Based on the assumption of a three month lockdown (with another three months of partial lifting), real GDP is expected to fall by 35% in Q2 2020, compared to Q1, with unemployment rising to 2m (10%), then declining as the economy slowly recovers. Looking at the table below, the OBR’s is the most pessimistic forecast, however, it also has to be noted that it is also the most recent.

In terms of annual GDP, this forecast represents a fall of 13%. Analysing the impact by sector, one of the hardest hit is not unexpectedly forecast to be the accomodation and food service sector.

With coronavirus affecting nearly every country throughout the world, each will suffer a similar impact, the extent of which, as we have seen, will depend on the policies of its government to first tackle the spread and then the steps it takes to kickstart the economy. Each has an extremely difficult balancing act to perform, first to control the virus and then second to minimise the damage to the long term prospects of its economy.

…unprecedented in recent times

Unfortunately, there are no precedents to guide decision making nor help us in making an accurate assessment, certainly at this relatively early stage, of the likely impact on world trade. Experience gained from the most similar example in recent history, the SARS outbreak in 2003, is of only limited use. China’s GDP at the time was increasing by 10% and that of the world by 4.3%. SARS had only a relatively minor impact on global trade, it was less contagious and caused fewer deaths. Coronavirus has hit us at a time when we are more vulnerable. World output grew by only 2.9% in 2019, the slowest since the 2008-9 crisis. China’s current share of global output is almost double its share from back in 2003, and it has accounted for over a third of the cumulative growth in global GDP since 2008.

We can only hope that the measures taken by individual countries stop the spread of the virus in the coming weeks, and that whilst suffering horrendously at the current time, economies sustain no irreparable damage. Also finally, that somehow, those same countries can work together to produce a co-ordinated response, initially to deal with the current challenges and then, just as importantly, to ensure we are all better prepared to deal with anything similar that arises in the future.

(First published 10 April 2020, with subsequent updates)

A few words about CompassAir

Creating solutions for the global maritime sector, CompassAir develops state of the art messaging and business application software designed to maximise ROI. Our software is used across the sector, including by Sale and Purchase brokers (S&P/SnP), Chartering brokers, Owners, Managers and Operators.

Through its shipping and shipbroking clients, ranging from recognised World leaders through to the smallest, most dynamic independent companies, CompassAir has a significant presence in the major maritime centres throughout Europe, the US and Asia.

Our flagship solution is designed to simplify collaboration for teams within and across continents, allowing access to group mailboxes at astounding speed using tools that remove the stress from handling thousands of emails a day. It can be cloud based or on premise. To find out more contact solutions@thinkcompass.io. If you are new to shipping, or just want to find out more about this exciting and challenging sector, the CompassAir Shipping Guide might prove to be an interesting read.

Contact us for more information or a short demonstration on how CompassAir can benefit your business, and find out how we can help your teams improve collaboration and increase productivity.